Our biggest achievement has been to help investors see the immense value in the process of financial planning

We are now three years old. And as is a practice every year, we are delighted to share the impact our financial planning and investment advisory platform has had. Given that the volume of data has multiplied over the years, it took us a while to collate and dig out all the details, but here we are.

We started Samasthiti with a simple idea – to provide honest financial planning services to everyone. Right from the beginning, we were sure that we wanted to build a client-centric advisory model. We knew that unless we catered to the real needs of the clients and helped them sort out their financial lives, we would not be contributing towards Samasthiti’s mission which is:

To democratize financial planning in India by providing unbiased and trustworthy financial services to everyone in need.

True to our mission, our model is based on two features. First, is to not take any commissions from financial product companies. We knew that taking commissions would come in the way of providing unbiased advise. Hence, Samasthiti’s entire revenue (every single penny of it) comes directly from our clients. This allows us to provide advise that is honest.

The second feature is to charge a transparent fixed fee for the services we provide and not determine the fees based on the portfolio size of our clients. A fixed fee, which is decided based on the work involved, prevents us from discriminating between low-income and high-income clients.

We are delighted to share with you the impact that Samasthiti has been able to make in the financial lives of our clients. Over the last three years, we have been able to,

Increase clients’ savings in mutual funds from an average of less than INR 20,000 per month to an average of about INR 94,000 per month

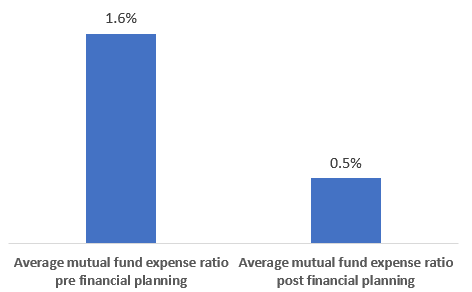

Reduce the annual cost of clients’ mutual fund portfolios from an average of 1.6 percent to 0.5 percent

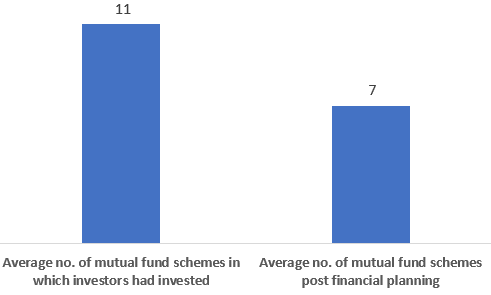

Streamline clients’ mutual fund portfolios by reducing exposure from an average of 11 mutual fund schemes to an average of 7 mutual fund schemes

Restrict clients’ exposure to cocktail investment products (that offer a multitude of benefits none of which is substantial) and get them to invest in simple but powerful investment products. For instance, more than half of our clients who did not have PPF accounts earlier, have now opened such an account and started contributing to it.

Multi-fold increase in investing

The most significant impact we have had is enabling a quantum leap in the monthly investment being made by our clients. This has not been achieved through a reduction in consumption spending, but simply by putting a plan which has enabled savings to be translated to investments. We had more and more clients with the same problem – a healthy savings rate, but with savings being accumulated in savings bank account or fixed deposits.

This is despite the fact that the clients had many long-term goals and were well placed to take equity-risk. Among our client base, the average investment in mutual funds prior to their financial planning was barely INR 20,000 per month. Post our financial planning, this figure zoomed up to about INR 94,000 per month.

In most cases, this staggering increase is the result of one thing–

Taking out time to think about what is happening to their money for the first time in their life.

Costs matter – a lot

Every financial product has a cost. This cost can be broken into two components – a part of the cost flows to the manufacturer of the financial product, and the other part to the intermediary who distributes the product in the market. Both these costs can cause a significant drain on the returns you earn as an investor.

We are extremely finicky about costs. The reason is obvious – every penny saved in costs immediately flows into earning a higher return from your portfolio. A saving of 1 percentage point per annum, compounded over say 15 years, leads to an additional return of more than 15 percent.

The average cost of our clients’ mutual fund portfolio was 1.6 percent per annum earlier, and this average has come down to 0.5 percent per annum post their financial planning exercise.

This corresponds to a savings of more than 1 percent annually. This saving was achieved by not only enabling our clients to invest directly in financial products, bypassing all intermediaries, but also by avoiding high-cost financial products.

Bringing down over-diversification

The way mutual funds are sold in India leads to investors significantly over-diversifying their portfolio. Every new mutual fund sale offer is marketed heavily on the back of fat commissions and is heavily marketed. This leads to investors jumping from one new fund offer to another, and very soon, their portfolio starts looking like a closet stuffed with a plethora of mutual funds – all mindlessly jumbled.

During the course of the last year, we witnessed portfolios – some with more than 40 different mutual fund schemes! The exposure to a large number of mutual fund schemes is also a reflection of an abject lack of clarity in designing one’s portfolio.

In our financial planning process, we pay special attention to cleaning messy mutual fund portfolios. Through careful analysis, we have been able to streamline our clients’ mutual fund holding from an average of 11 different schemes to an average of 7 different schemes.

Simple is Powerful

Cocktail financial products are those that combine multiple objectives. The most common cocktail products are those that combine investment and insurance, like Unit-Linked-Insurance-Plans (ULIPs) or traditional LIC policies. Such products are a marketers’ delight as the product complexity allows for innovative but obfuscating packaging. Such products, though, struggle to achieve any of their objectives.

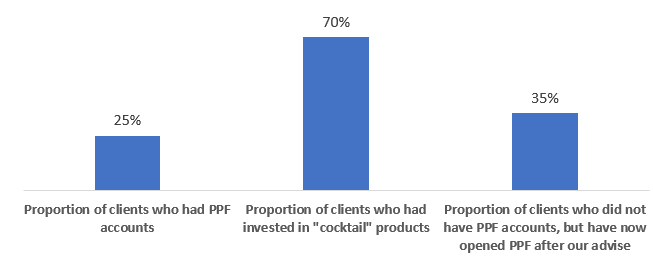

What is worse, the cocktail nature of their design provides a cover for charging high fees. These high fees enable the manufacturer of such products to pay attractive commissions on their sale. Little surprise then that an average retail investor’s portfolio will have a decent sprinkling of cocktail financial products. Among our client base, more than 70 percent of them either had an investment in a ULIP or a LIC policy.

Compare this to the fact that only about 25 percent of our clients had a Public Provident Fund (PPF) account when they approached us. This is despite the fact that PPF is one of the best investments you can make. Unfortunately, the simplicity of PPF is perceived as being boring, rather than being interpreted as its strength. Nobody wants to talk about PPF as there is no commission to be made on getting people to open PPF accounts. At Samasthiti, we strongly advise our clients, where applicable, to open a PPF account and contribute to it regularly.

Close to half our clients who did not earlier have PPF accounts, have now opened such an account and started contributing to it.

Thank you

None of all this would have been possible without the trust and support of our clients and well-wishers, and for this, we will be eternally grateful.

In 2022, we launched our much-anticipated Samasthiti Life program which allows investors to make sure that every actionable in their financial plan gets executed. The Samasthiti Life program also allows investors to be in deeper touch with their financial plan and make sure it always remains updated.

We would be delighted to get you started on your financial planning journey. Click on the link below and we will get in touch with you!

0 Comments