This post is based on our research study titled “Boosting Retirement Income through Dynamic Withdrawals” which can be accessed here.

The most common withdrawal style from a retirement portfolio is to withdraw a fixed amount and increase that amount annually by inflation. This is the classic “constant inflation-adjusted withdrawal”, often also called the Bengen-style approach (in our research study, we label it as “Baseline”). It is simple, predictable, and gives you the same purchasing power year after year.

The key point to note in the Bengen-style approach is that the only variation in your withdrawals comes from inflation. The withdrawal does not react to changes in your retirement corpus due to market movements. Such withdrawal methodologies are called “static withdrawals”.

If you have heard of the 3-4% safe withdrawal rate, it refers to the withdrawal rate for static approaches like the Bengen-style approach. A key question arises – what happens to withdrawal rates when we move away from the Bengen‑style approach?

There are several dynamic withdrawal approaches where withdrawals not only change with inflation but also adjust to changes in your retirement corpus. In this post, we will evaluate one such dynamic withdrawal option, the forego-inflation approach.

What Is the Forego Inflation Strategy?

The forego inflation rule is a small but powerful modification to the Bengen-style approach. The rule states that you get your annual inflation raise only if your portfolio has grown in value over the past year. If the portfolio has declined or stayed flat, you simply skip the inflation adjustment and withdraw the same nominal amount as the previous year.

Imagine you retired with a corpus of ₹1 crore and started withdrawing ₹3.2 lakh per year (a 3.2% withdrawal rate). If inflation is 5% and your portfolio has grown, your next year’s withdrawal rises to ₹3.36 lakh. But if the portfolio dropped in value you will continue withdrawing ₹3.2 lakh. No raise, but no cut either.

Every skipped inflation adjustment means your real (inflation-adjusted) income quietly erodes a little. In exchange, you are drawing less from a stressed portfolio, giving it more room to recover. It’s a form of belt-tightening that happens automatically, without requiring you to make difficult decisions about cutting your spending.

A Realistic Example

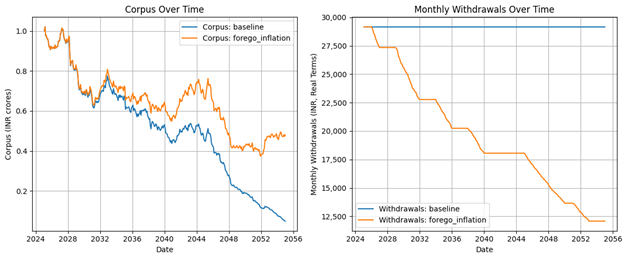

To see how the forego-inflation rule might behave, we randomly generated a sequence of market returns and inflation rates. The left panel of Figure 1 tracks what happens to the corpus over time under both the forego-inflation rule and the constant inflation-adjusted withdrawals (Bengen-style approach or Baseline). The right panel tracks monthly withdrawals, adjusted for inflation (reflecting actual purchasing power).

Figure 1: Forego Inflation Rule vs. Baseline (Constant Inflation-Adjusted Withdrawals)

Source: Saraogi, R. (2025). Boosting Retirement Income through Dynamic Withdrawals

Note: In the forego inflation rule, real withdrawals are not increased in years following a portfolio decline. This leads to gradually declining inflation-adjusted income but helps preserve corpus over time, especially in volatile market periods.

The results over a 30-year horizon are striking. The baseline strategy, where withdrawals are consistently inflation-adjusted regardless of market performance, depletes the corpus entirely by around 2055. The forego inflation portfolio, by contrast, survives the full period with roughly 50% of the original corpus still intact.

However, this retention of the original corpus under forego-inflation rule comes at a cost. In the right panel, you can see a gradual stepdown in real withdrawals, from around ₹26,000 per month to under ₹10,000 by the end, as skipped inflation adjustments compound over decades.

A Closer Look at Performance Metrics

When evaluating dynamic withdrawal strategies, like the forego inflation rule, just looking at failure rate alone is not adequate. The traditional way of evaluating withdrawal strategies by asking “what percentage of simulations ran out of money?”, was designed for static rules and breaks down when applied to dynamic ones.

A strategy that slashes your income by 60% to keep the portfolio alive technically “succeeds” by the failure rate metric, but in practical terms, it’s a failure since the retiree may not be able to cover for basic expenses with such significant cut in withdrawals.

Therefore, to properly evaluate dynamic strategies, we need a multi-dimensional lens. In our research, we developed an evaluation framework built around four dimensions:

- Spending – how much income does the strategy actually deliver over time?

- Stability – how volatile is that income from year to year?

- Savings – how much wealth remains at the end for legacy or emergencies?

- Sustainability – what is the risk of the plan failing?

In the articles ahead, including this one, we will evaluate dynamic withdrawal strategies through all four of these lenses.

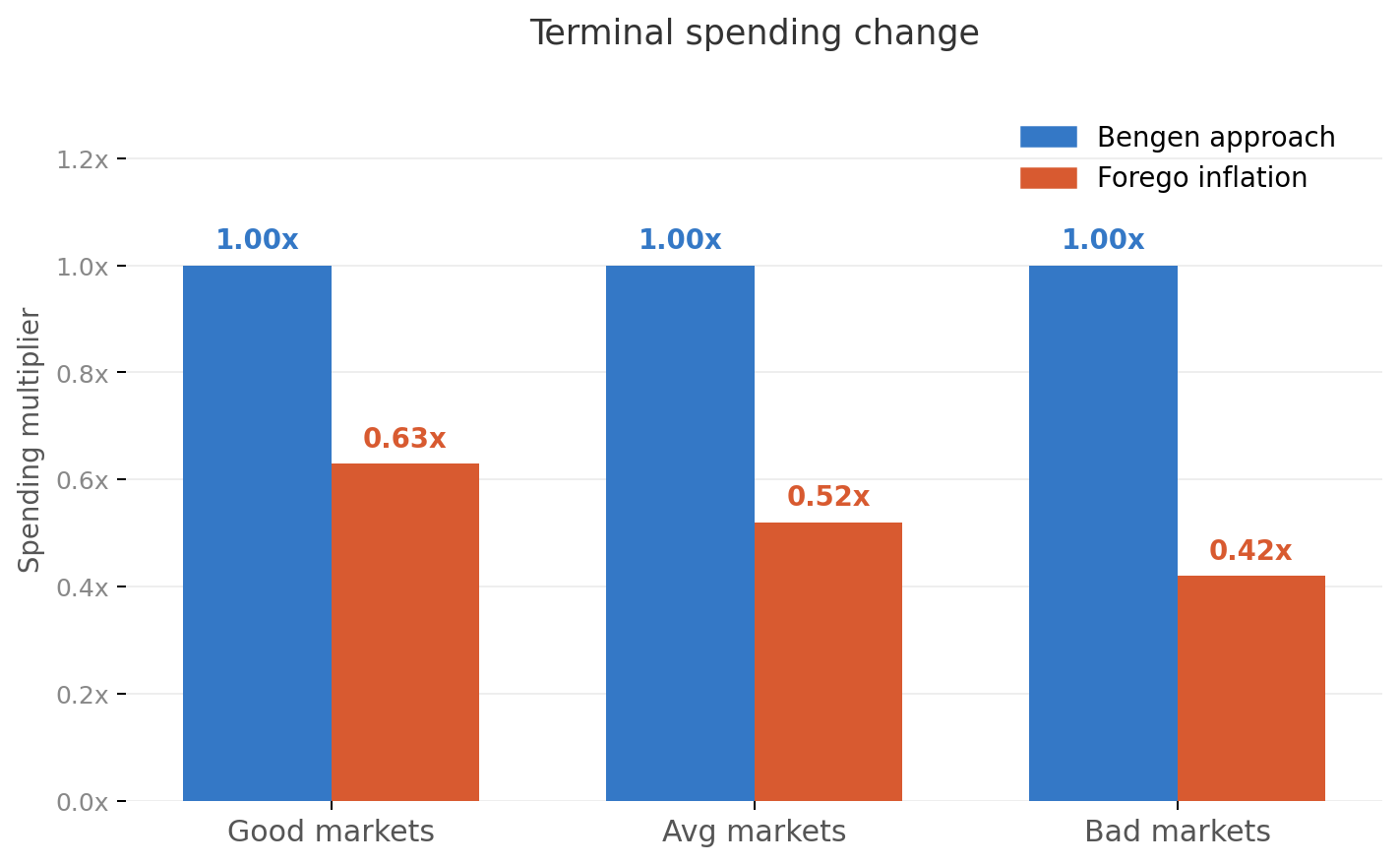

Spending: Lower Over Time, by Design

As the forego-inflation strategy frequently skips inflation adjustments, real withdrawals decline steadily. The Bengen-style or constant inflation adjustment approach maintains the same real spending power throughout retirement, holding at 1.0x regardless of market conditions. The forego inflation strategy, by contrast, steadily erodes real income over time.

Terminal Spending Change – How spending changes at the end of retirement compared to start of retirement

Source: Saraogi, R. (2025). Boosting Retirement Income through Dynamic Withdrawals

Note: Terminal spending change measures how much your real (inflation-adjusted) withdrawal in year 30 has changed compared to what you started with at retirement. A value of 1.0 means your purchasing power is the same as day one you are still withdrawing the equivalent of your original amount in today’s money.

A value below 1.0, say 0.52, means your real withdrawal has fallen to just 52% of what it was when you retired — so even though the nominal rupee amount hitting your account may look similar, it buys significantly less than it used to. It is calculated as: Terminal Spending Change = Spending in Year 30 / Spending in Year 1

Even in good markets, you end up spending (in year 30) only 63% of your starting income in real terms. In average markets, this falls to 52%, and in bad markets, just 42%. The bottom line is that under the forego-inflation rule, your real spending can see a significant cut.

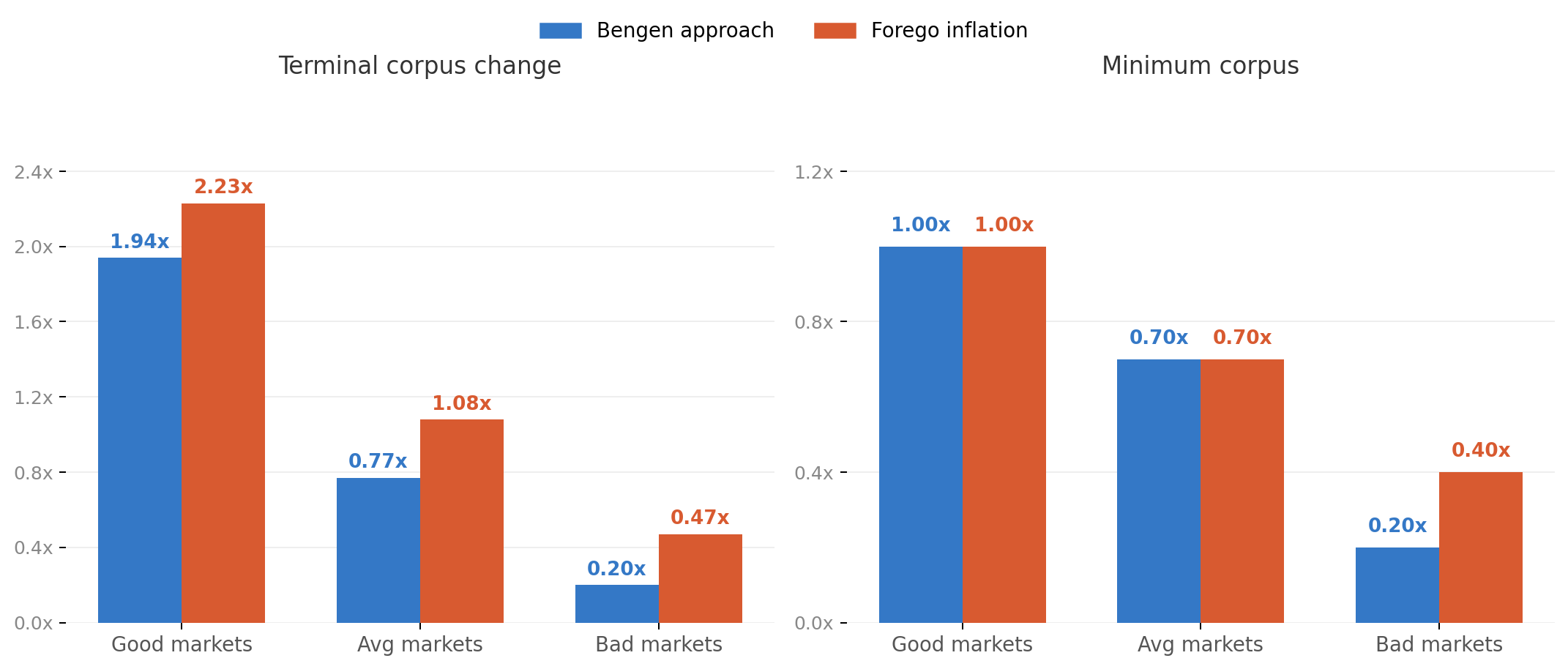

Savings: Excellent for Preserving Your Corpus

When it comes to preserving your retirement corpus, the forego-inflation strategy outshines. In good markets, the forego inflation strategy ends 30 years with 2.23x the starting corpus, outpacing the Bengen-approach’s 1.94x. This is the compounding effect of consistently drawing less. Every skipped inflation adjustment leaves more in the portfolio to grow.

In average markets, the contrast is starker. While the Bengen-approach ends with just 0.77x of the starting corpus, meaning the portfolio has shrunk, the forego-inflation ends at 1.08x — the portfolio has actually grown. And in bad markets, the Bengen-approach leaves only 0.20x of the original corpus intact, while forego-inflation preserves 0.47x.

How well is the retirement corpus preserved?

Source: Saraogi, R. (2025). Boosting Retirement Income through Dynamic Withdrawals

Note: (1) Terminal corpus change measures the value of your portfolio at the end of 30 years relative to what you started with. A value of 1.0 means the corpus is exactly the same size as when you retired, a value above 1.0 means it has actually grown, and a value below 1.0 means it has shrunk. So a terminal corpus change of 0.77 means you end retirement with only 77% of what you started with, while a value of 2.23 means your portfolio has more than doubled over the same period.

(2) Minimum corpus captures the lowest point your portfolio touches at any time during the entire 30-year retirement. It is expressed as a proportion of your starting corpus, so a value of 0.4 means your portfolio fell as low as 40% of its starting value at some point — even if it recovered later. This metric matters because a deep portfolio drop mid-retirement can be psychologically distressing and may force difficult decisions, even if the strategy ultimately survives.

The metric ‘minimum corpus’ reinforces this story. In good and average markets, both strategies hold the portfolio floor at the same level, but in bad markets the divergence is clear — 0.4x versus 0.2x at the lowest point. This matters enormously in practice. A retiree on the Bengen approach could find their portfolio halved and still falling, triggering panic or forced changes. The forego inflation retiree, drawing less through the downturn, never falls that far. The strategy’s conservatism, which felt like a sacrifice in the spending charts, turns out to be powerful insurance for the corpus.

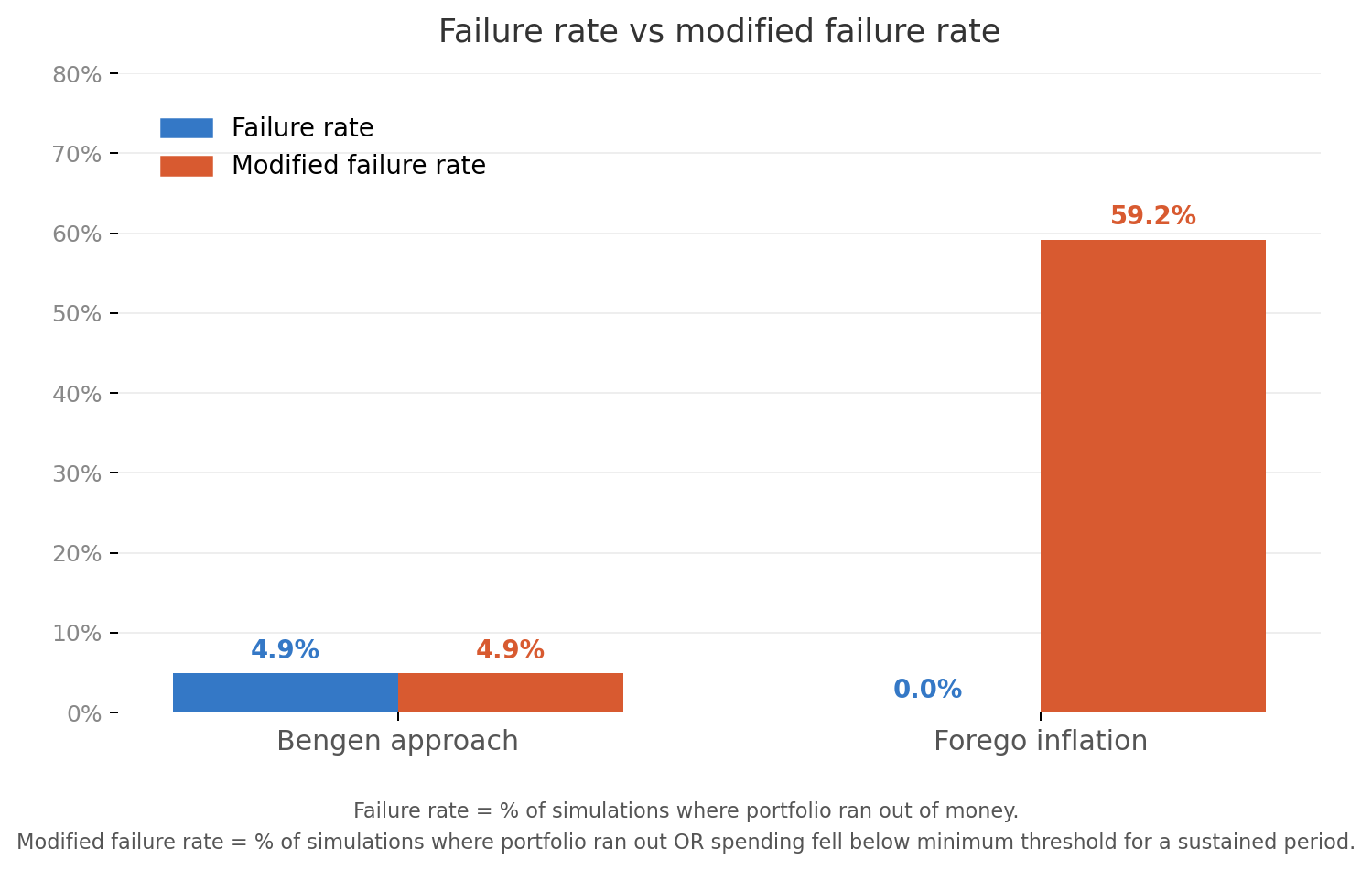

Sustainability: Eliminates Portfolio Ruin, But Introduces a Different Kind of Failure

The traditional failure rate is a simple measure that asks what percentage of simulations result in the portfolio running out of money before the end of retirement. It is the classic way of evaluating withdrawal strategies and works well for static approaches like the Bengen-approach.

The modified failure rate is a more nuanced metric, developed to address a key blind spot in the traditional measure. A dynamic strategy that slashes your withdrawals by 50% to keep the portfolio alive technically “succeeds” by the traditional measure as the money never runs out, but in practice, the retiree may no longer be able to cover basic expenses. The modified failure rate captures this by also counting simulations where there is a material erosion of living standards as a failure, even if the corpus itself survives.

Together, the two metrics, the traditional failure rate and the modified failure rate, give us a much fuller picture of whether a strategy is truly sustainable.

The Bengen-approach carries a 4.9% traditional failure rate. The modified failure rate is identical at 4.9%, because spending never falls in this approach. The forego-inflation strategy flips this picture completely. Its traditional failure rate is 0%, which means the portfolio essentially never runs out, because by consistently drawing less during down years, the retiree never overdraws a stressed portfolio to the point of depletion. This is a fantastic achievement.

However, the modified failure rate is significantly higher at 59.2%. The modified failure rate captures simulations where there is a prolonged and material erosion of living standards. The bottom line here is that under the forego-inflation rule, your money won’t run out, but your income might erode to a point where it no longer supports your lifestyle adequately.

Failure rates – Did the corpus last for the entire retirement period?

A higher starting income — but at a cost

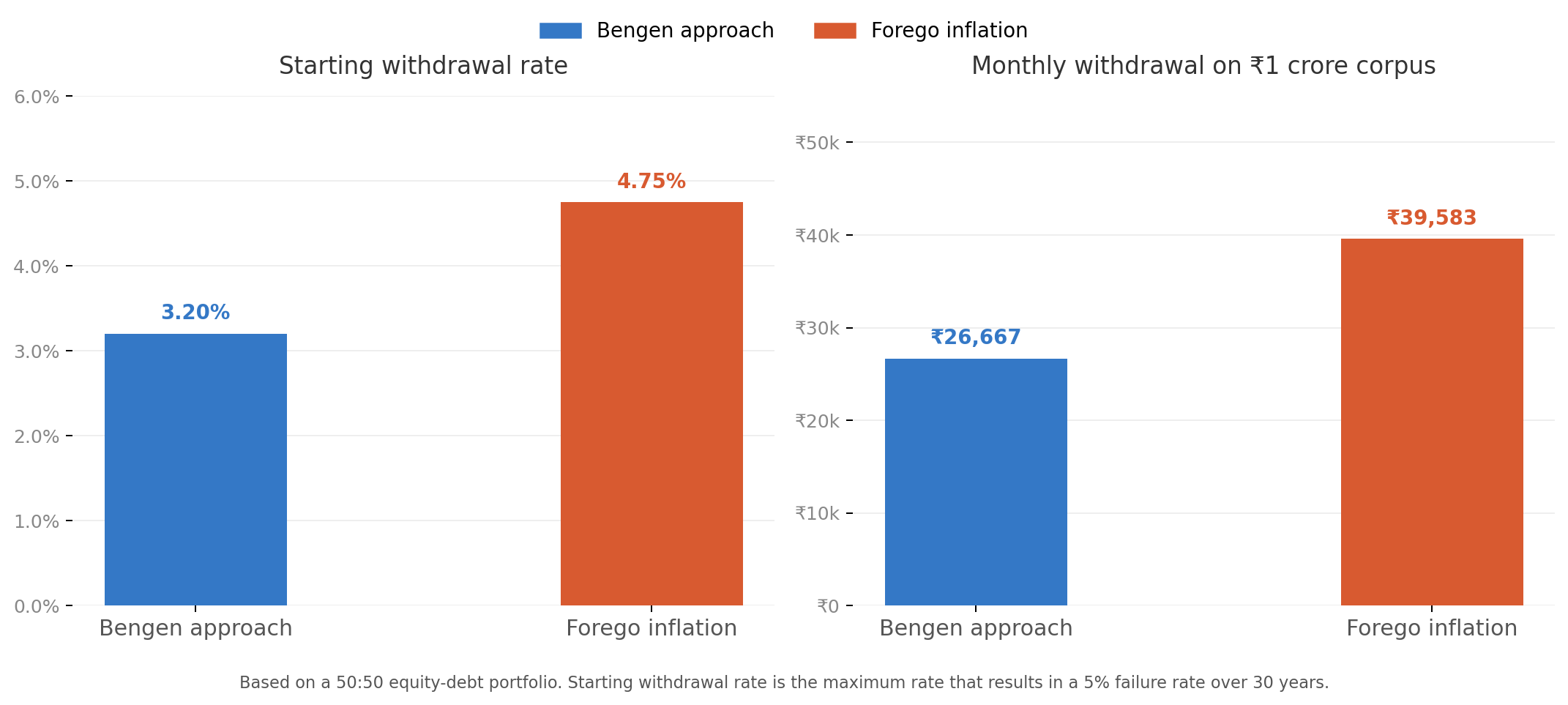

One huge benefit of forego-inflation strategy is that it allows retirees to start with a higher initial withdrawal rate than the Bengen-approach. Because the strategy self-corrects during downturns by skipping inflation raises, the portfolio is less likely to deplete, which means it can safely absorb a higher starting withdrawal. For a broadly balanced equity-debt portfolio, our research shows the safe withdrawal rate under the forego inflation approach is around 4.75%, compared to 3.2% for the Bengen-approach.

In rupee terms, for a ₹1 crore retirement corpus, this translates to a meaningful difference. Under the Bengen-approach, a retiree would start with annual withdrawals of ₹3.2 lakh, or roughly ₹26,667 per month. Under the Forego Inflation strategy, the same retiree could start with ₹4.75 lakh per year, or approximately ₹40,000 per month — about ₹15,000 more every month from day one.

Forego-inflation approach allows for higher starting withdrawals

Source: Saraogi, R. (2025). Boosting Retirement Income through Dynamic Withdrawals

However, this higher starting income comes with an important caveat. As we saw earlier, the forego-inflation strategy progressively erodes real withdrawals over time. So, while you begin retirement with more in hand, that advantage gradually reverses as skipped inflation adjustments compound over the years. The higher starting rate is real, but it should not be read as a free upgrade.

Who Is This Strategy For?

The forego inflation strategy isn’t for everyone, but it fits certain retiree profiles well. It’s a good fit if you prioritize capital preservation above all else, perhaps because you want to leave a legacy, or because you have other income sources (pension, rental income) that cover your essentials and your corpus is primarily a safety net. It also suits retirees who are deeply uncomfortable with the idea of their portfolio running out and are willing to accept a declining standard of living in exchange for that security.

It’s probably not the right choice if you depend entirely on your retirement corpus for daily expenses, especially non-discretionary ones like healthcare and housing. The gradual erosion of purchasing power can become significant over your retirement years.

Conclusion

The forego inflation strategy is the gentlest possible introduction to dynamic withdrawals. It asks very little of the retiree, just a willingness to occasionally forgo an inflation raise, and in return, it provides strong portfolio preservation and zero risk of outright depletion.

But that simplicity comes at a real cost. Our analysis shows clearly that this is a strategy that prioritizes the longevity of your money over the longevity of your lifestyle. If you have other income sources, the forego inflation strategy can serve as a powerful backstop, quietly preserving your corpus while your other income does the heavy lifting.

But if your retirement portfolio is your primary source of income, the gradual erosion of purchasing power it produces is a significant inconvenience. The forego inflation rule is a good starting point, but for most retirees, the journey into dynamic withdrawals need not stop here.

We will in subsequent posts cover more dynamic withdrawal strategies that retirees can evaluate.

This article is based on research that uses Indian market data and is for informational purposes only. It does not constitute investment advice. Please consult your financial advisor before making any investment decisions.

0 Comments