This article is based on our research titled “Boosting Retirement Income through Dynamic Withdrawals” and can be accessed here

You’ve saved diligently for decades and built a retirement corpus. Now comes the important question – how do you actually take money out of it?

This is the withdrawal problem, and it turns out to be far harder than the accumulation problem that preceded it. The retirement planning world has been grappling with this question for over three decades, and the answer has evolved from a single and simple withdrawal rule into a diverse set of options.

A retiree today needs to make a fundamental choice. Do you want a static withdrawal plan that gives you the same real income every year, or a dynamic one that adjusts with market conditions?

The Static Approach: Predictable, but Rigid

The most famous static withdrawal rule is the constant inflation-adjusted withdrawal, sometimes called the “4% rule” after William Bengen’s pioneering 1994 research. The idea is simple. Withdraw a fixed percentage of your initial corpus in year one (say, 3.2% for a typical Indian retiree), then increase that amount by inflation every year, regardless of what the market does.

If you retire with ₹1 crore, you withdraw ₹3.2 lakh in year one. If inflation is 5%, you withdraw ₹3.36 lakh in year two. ₹3.53 lakh in year three and so on. This allows your real purchasing power to stay constant.

The appeal of this static withdrawal style is the predictability. You know that you can adjust your withdrawal with inflation each year and maintain your lifestyle. It’s the closest thing to a pension that a self-funded retiree can create. Our research on the Indian markets suggests that a withdrawal rate of around 3.0-3.5% can sustain a 30-year retirement with reasonable safety.

But this predictability hides two serious problems.

In bad markets, the static rule ignores reality. Your portfolio could be down 30%, but you’re still withdrawing the same inflation-adjusted amount. You’re pulling money from a shrinking pool, accelerating the decline. If poor returns persist for several years early in retirement, the dreaded “sequence-of-returns risk” can lead to portfolio depletion with no mechanism to course-correct.

Also, in good markets, the static rule leaves money on the table. If your portfolio doubles over a decade of strong returns, you’re still withdrawing based on what you started with. You end up underspending throughout retirement and leaving behind a large, unintentional legacy.

The Dynamic Approach: Adaptive, but Volatile

Dynamic withdrawal strategies emerged as a response to these limitations. The core idea is to let your withdrawals respond to how your portfolio is actually performing. When markets do well, you can spend a bit more. When they struggle, you pull back.

There are many flavours of dynamic withdrawals, from simple rules like skipping an inflation raise after a bad year, to sophisticated approaches like the Guardrails method, the Zolt glide path, or endowment-style moving averages. But they all share the common trait of trading certainty of a fixed real income stream for the flexibility of an adaptive one.

This flexibility carries a tangible benefit. Dynamic strategies can pull back spending during downturns, thereby protecting the portfolio from the worst effects of sequence-of-returns risk. A retiree who reduces withdrawals by even a small amount after a market crash gives their portfolio crucial breathing room to recover. Over a 30-year horizon, this can be the difference between ruin and comfort.

Can Dynamic Strategies Let You Withdraw More?

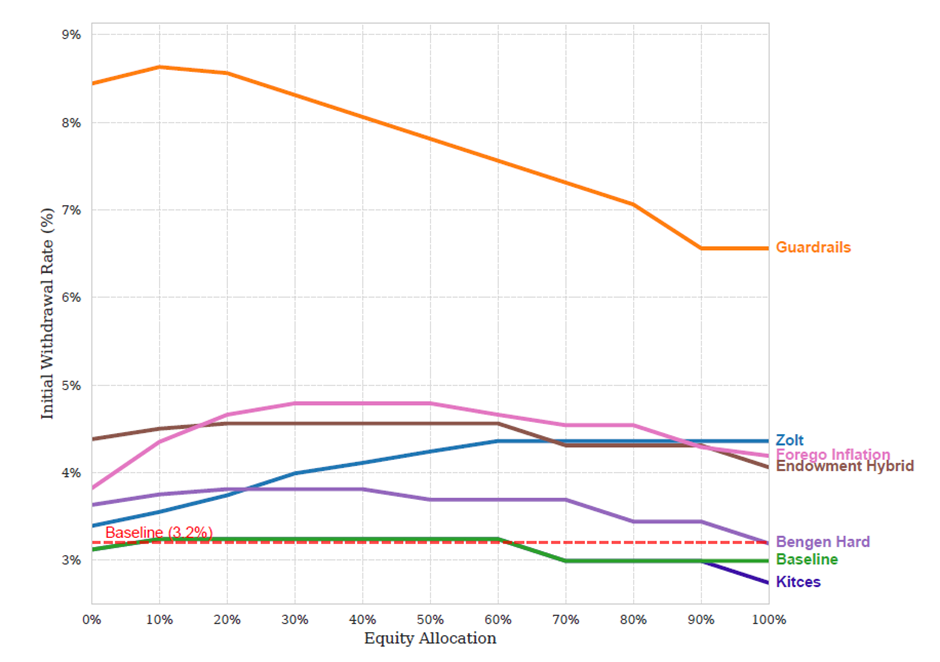

If dynamic strategies are better at protecting the portfolio, can they also support a higher starting withdrawal rate? Our research explored this question directly and the answer is presented in the chart below.

Safe withdrawal rates by withdrawal strategy and equity allocation

Source: Samasthiti Advisors. Note: The static approach, which is the Bengen-style withdrawal has been shown as “Baseline”. Starting withdrawal rates under Dynamic strategies typically sit above the Baseline.

Most dynamic strategies do allow a higher starting withdrawal rate, typically landing in the 3.5% to 4.8% range depending on the strategy and equity allocation.

Approaches like the Zolt glide path, Forego Inflation, and Endowment Hybrid cluster around 4.5% at balanced equity allocations.

The Guardrails strategy stands out dramatically, supporting initial withdrawal rates of 7-9%. But this comes with a major caveat that the Guardrails approach can also dramatically cut withdrawals during bad markets. You can start higher, but you might have to endure very lean years.

The Real Trade-off: Spending Level vs. Spending Stability

The deeper insight from our research is that dynamic strategies don’t just shift the withdrawal rate but fundamentally change the character of retirement income. The trade-off isn’t simply higher versus lower withdrawal rates, but between different kinds of retirement experience.

Static strategies offer high year-to-year stability. Your withdrawal income moves perfectly and predictable with inflation but since the withdrawals do not react to corpus movements, our research shows that the static baseline at 3.2% initial withdrawal has a roughly 5% failure rate, and when it fails, the shortfall is severe.

Dynamic strategies offer resilience and adaptability. They can virtually eliminate the risk of complete portfolio depletion. But they introduce income volatility and your withdrawals will fluctuate, sometimes significantly. In bad market periods, some strategies can see real income drop to 40-50% of the starting level by year 30.

What This Means for Indian Retirees

The key takeaway is not that one approach is universally better but you need to understand what you’re choosing. A static plan gives you certainty but at the cost of a failure probability, albeit small. A dynamic plan gives you more spending power, but at the cost of predictability.

In the articles that follow in this series, we’ll examine specific dynamic strategies one by one. We will explore how they work, how they performed in Indian market simulations, and who they’re best suited for. Understanding the landscape of options is the first step toward picking the right one for your retirement.

This article is based on our research that uses Indian market data and is for informational purposes only. It does not constitute investment advice. Please consult your financial advisor before making any investment decisions.

0 Comments